The Borrowing Money Guide is where you can find all of the information that you need to make smart decisions about loans and mortgages. Borrowing money is one of the most important concepts in personal finance because a loan will have a big impact on your finances. I will break down the types of loans and mortgages available to consumers and in some cases, highlight their features. Navigating the loan and mortgages market can get confusing, especially because there are so many options to choose from.

Who Can I Borrow Money From?

There are several financial institutions which offer loans and mortgages at various rates and for various purposes. The first step is to be clear about why you want to borrow money. If you are interested in purchasing a vehicle, mortgage rates would not be of interest to you. You also have to be clear about how much money you can borrow. Your salary, current financial commitments and age will impact your ability to borrow money.

When borrowing money, you can choose from commercial banks, credit unions, insurance companies, governmental agencies, small loan financiers and family. It is up to you to decide which one offers the best deals that will suit your situation. When looking at the details of the loan or mortgage, look at the loan amount, payback period, interest rate, service charges and clauses that allow you to pay back the loan early.

Vehicle Loans

Looking for a new or used car? Search for competitive rates and flexible payment terms before deciding on a loan. The requirements for purchasing new and used vehicles may differ, depending on which institution you go to. Loans for used vehicles are a bit more strict and may require additional documentation. Purchasing a car is a big step that should be done with careful consideration. In addition to paying for your car, you will have to budget for monthly and annual carrying costs which include gas, insurance, taxes and repairs and maintenance.

Education Loans

Now is always the right time to study. However, you have to choose how to pay for your education carefully. Education loans are offered by several types of financial institutions. Some financiers require you to start your repayment as soon as the loan has been approved. Others allow you to complete your studies first and may even offer a grace period on completion. Student loans may require guarantors who will be responsible for paying back your loan in the event that you default. Some institutions allow a grace period after completion of your studies.

Home Equity Loans

A home equity loan allows customers to borrow against the value of your home to facilitate a purchase or investment. Funds can be used for personal expenses including travel, education and medical expenses. Home equity loans are attractive because they have good interest rates and they are easy to apply for and obtain approval. They are also popular because they allow home owners to borrow using the equity in the home as collateral.

Home Improvement Loans

As a home owner, you are tasked with the responsibility of maintaining your home. It does not make sense to have an asset like your home and not keep it in the best condition possible. You can use a home improvement loan to increase your home’s efficiency andAss increase its curb appeal in the event that you have to sell it or make an addition to increase its comfort and space. Unlike the home equity loan, the home improvement loan is a type of personal loan and does not require your home’s equity as collateral.

Land Loans

It’s always good when people invest their money in an asset that will appreciate over time. Land is a good example of one of those assets. When you purchase land, you have several options for constructing your home. You can build your home in stages using cash and smaller loans; apply for the mortgage whilst paying for the loan or you can wait until the land is paid off before applying for a mortgage or loan. When purchasing land, you should have some idea of the type of property you want to build as well as the covenants for the land and the neighbourhood.

Lines of Credit

A line of credit can be a flexible and convenient method to access credit usually in the form of cash. It is an agreement between a lender and a borrower in which the lender gives the borrower a maximum loan balance. The borrower can access these funds at any time, but can not withdraw more that the agreed amount. Lines of credit are popular because you just have to apply once, the cash is always available to you and you only pay interest on the outstanding balance. Just remember that with lines of credit there is a minimum amount you have to pay each month.

Mortgages

If you’re looking to purchase or build a home, but you do not have the cash, you can consider a mortgage. A mortgage is a loan facility where the buyer gets money from a lender to purchase a property. The buyer must repay the lender an agreed amount within an agreed period of time. Mortgages have their advantages and disadvantages, so you have to research them thoroughly. One major advantage of the mortgage is that its a route to home ownership, a dream that many people have. However, with a mortgage, the loan interest will dramatically impact your payback and the payback period.

Credit Cards

A credit card is a type of loan which allows people to borrow money from a lending institutions for smaller purchases. Credit cards are unsecured loans which are characterised by higher interest rates and a short payback period of less than thirty days. Some credit cards are rewards driven and users can enjoy cash back on purchases and points which can be redeemed for travel or new purchases. Credit cards are convenient, can facilitate online shopping and are thought to be safer that carrying cash. However, borrowers should be cautious when using credit cards, because it’s very easy to overspend.

Payday Loans

Another method of borrowing money is the payday loan or a cash advance loan. It is a short-term loan designed to help you to pay immediate expenses. The difference between a payday loan and other loans is that the payback period is usually a couple days or until your next payday. Finance charges are usually higher than other loans and if the loan is not repaid by the next payday, the charges increase. Payday loans may also require borrowers to provide access to their accounts or write a cheque to the lender for the amount owed.

Title Loans

With a title loan, you have to sign over the title of you car in exchange for the cash that you need. If you do not pay back the loan, then the lender has the power to keep your car. Title loans are very controversial because of the high interest rates and the fees. Although they are short term loans, they are also very risky because if you miss one payment you can lose your vehicle.

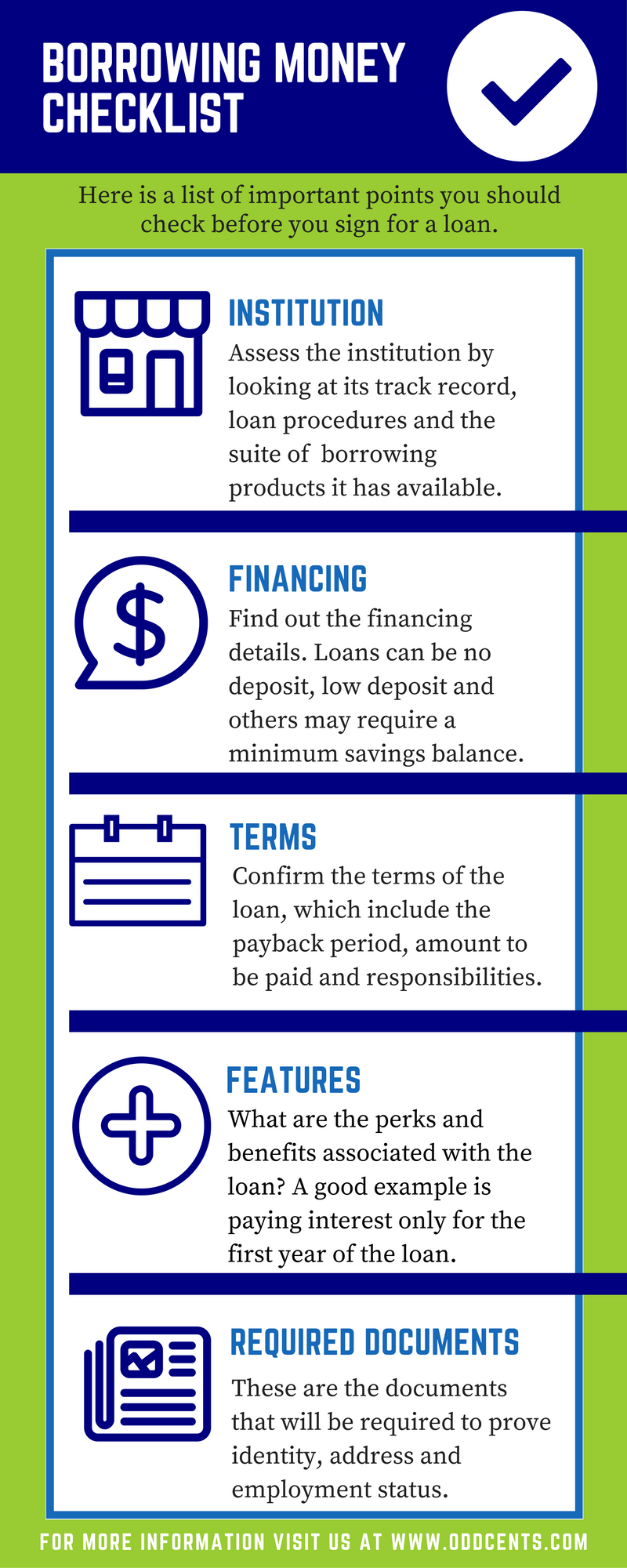

Borrowing Money Guide Checklist

These are only some of the loans that are available. Other loans may fall under the categories of personal loans, consumer loans and general purpose loans. When deciding on the type of loan that is suitable for you, thorough research will be helpful.

The checklist below details a few things you should bear in mind when borrowing money. It does not make sense signing up for a loan when you’re not sure about what you are doing. Always sign a loan with a clear head and only after you have asked all of the pertinent questions.

To learn more about how Odd Cents can help you, check out our Recommendations or visit the blog.

Share this Borrowing Money Guide on Facebook where you can join discussions on hot topics.